Nº 2665 - Fevereiro/Março de 2024

Pessoa coletiva com estatuto de utilidade pública

Last year’s Global Risks Report warned of a world that would not easily rebound from continued shocks. As 2024 begins, the 19th edition of the report is set against a backdrop of rapidly accelerating technological change and economic uncertainty, as the world is plagued by a duo of dangerous crises: climate and conflict.

Underlying geopolitical tensions combined with the eruption of active hostilities in multiple regions is contributing to an unstable global order characterized by polarizing narratives, eroding trust and insecurity. At the same time, countries are grappling with the impacts of record-breaking extreme weather, as climate-change adaptation efforts and resources fall short of the type, scale and intensity of climaterelated events already taking place. Cost-of-living pressures continue to bite, amidst persistently elevated inflation and interest rates and continued economic uncertainty in much of the world. Despondent headlines are borderless, shared regularly and widely, and a sense of frustration at the status quo is increasingly palpable. Together, this leaves ample room for accelerating risks – like misinformation and disinformation – to propagate in societies that have already been politically and economically weakened in recent years.

Just as natural ecosystems can be pushed to the limit and become something fundamentally new; such systemic shifts are also taking place across other spheres: geostrategic, demographic and technological. This year, we explore the rise of global risks against the backdrop of these “structural forces” as well as the tectonic clashes between them. The next set of global conditions may not necessarily be better or worse than the last, but the transition will not be an easy one.

The report explores the global risk landscape in this phase of transition and governance systems being stretched beyond their limit. It analyses the most severe perceived risks to economies and societies over two and 10 years, in the context of these influential forces. Could we catapult to a 3oC world as the impacts of climate change intrinsically rewrite the planet? Have we reached the peak of human development for large parts of the global population, given deteriorating debt and geo-economic conditions? Could we face an explosion of criminality and corruption that feeds on more fragile states and more vulnerable populations? Will an “arms race” in experimental technologies present existential threats to humanity?

These transnational risks will become harder to handle as global cooperation erodes. In this year’s Global Risks Perception Survey, two-thirds of respondents predict that a multipolar order will dominate in the next 10 years, as middle and great powers set and enforce – but also contest – current rules and norms. The report considers the implications of this fragmented world, where preparedness for global risks is ever more critical but is hindered by lack of consensus and cooperation. It also presents a conceptual framework for addressing global risks, identifying the scope for “minimum viable effort” for action, depending on the nature of the risk.

The insights in this report are underpinned by nearly two decades of original data on global risk perception. The report highlights the findings from our annual Global Risks Perception Survey, which brings together the collective intelligence of nearly 1,500 global leaders across academia, business, government, the international community and civil society. It also leverages insights from over 200 thematic experts, including the risk specialists that form the Global Risks Report Advisory Board, Global Future Council on Complex Risks, and the Chief Risk Officers Community. We are also deeply grateful to our long-standing partners, Marsh McLennan and Zurich Insurance Group, for their invaluable contributions in shaping the themes and narrative of the report. Finally, we would like to express our gratitude to the core team that developed this report – Ellissa Cavaciuti-Wishart, Sophie Heading and Kevin Kohler – and to Ricky Li and Attilio Di Battista for their support.

The future is not fixed. A multiplicity of different futures is conceivable over the next decade. Although this drives uncertainty in the short term, it also allows room for hope. Alongside global risks and the era-defining changes underway lie unique opportunities to rebuild trust, optimism and resilience in our institutions and societies. It is our hope that the report serves as a vital call to action for open and constructive dialogue among leaders of government, business and civil society to take action to minimize global risks and build upon long-term opportunities and solutions.

Saadia Zahidi

Managing Director

The Global Risks Perception Survey (GRPS) has underpinned the Global Risks Report for nearly two decades and is the World Economic Forum’s premier source of original global risks data. This year’s GRPS has brought together leading insights on the evolving global risks landscape from 1,490 experts across academia, business, government, the international community and civil society. Responses for the GRPS 2023-2024 were collected from 4 September to 9 October 2023.

“Global risk” is defined as the possibility of the occurrence of an event or condition which, if it occurs, would negatively impact a significant proportion of global GDP, population or natural resources. Relevant definitions for each of the 34 global risks are included in Appendix A: Definitions and Global Risks List.

The GRPS 2023-2024 included the following components:

– Risk landscape invited respondents to assess the likely impact (severity) of global risks over a one-, two- and 10-year horizon to illustrate the potential development of individual global risks over time and identify areas of key concern.

– Consequences asked respondents to consider the range of potential impacts of a risk arising, to highlight relationships between global risks and the potential for compounding crises.

– Risk governance invited respondents to reflect on which approaches have the most potential for driving action on global risk reduction and preparedness.

– Outlook asked respondents to predict the evolution of key aspects underpinning the global risks landscape.

Refer to Appendix B: Global Risks Perception Survey 2023-2024 for more detail on the methodology.

To complement GRPS data on global risks, the report also draws on the World Economic Forum’s Executive Opinion Survey (EOS) to identify risks that pose the most severe threat to each country over the next two years, as identified by over 11,000 business leaders in 113 economies. When considered in context with the GRPS, this data provides insight into local concerns and priorities and points to potential “hot spots” and regional manifestations of global risks. Refer to Appendix C: Executive Opinion Survey: National Risk Perceptions for more details.

Finally, the report integrates the views of leading experts to generate foresight and to support analysis of the survey data. Contributions were collected from 55 colleagues across the World Economic Forum’s platforms. The report also harnesses qualitative insights from over 160 experts from across academia, business, government, the international community and civil society through community meetings, private interviews and thematic workshops conducted from May to October 2023. These include the Global Risks Advisory Board, Global Future Council on Complex Risks and the Chief Risks Officers Community. Refer to Acknowledgements for more detail.

The Global Risks Report 2024 presents the findings of the Global Risks Perception Survey (GRPS), which captures insights from nearly 1,500 global experts. The report analyses global risks through three time frames to support decision-makers in balancing current crises and longer-term priorities. Chapter 1 explores the most severe current risks, and those ranked highest by survey respondents, over a two-year period, analysing in depth the three risks that have rapidly accelerated into the top 10 rankings over the two-year horizon. Chapter 2 focuses on the top risks emerging over the next decade against a backdrop of geostrategic, climate, technological and demographic shifts, diving deeper into four specific risk outlooks. The report concludes by considering approaches for addressing complex and non-linear aspects of global risks during this period of global fragmentation. Below are the key findings of the report.

A deteriorating global outlook

Looking back at the events of 2023, plenty of developments captured the attention of people around the world – while others received minimal scrutiny. Vulnerable populations grappled with lethal conflicts, from Sudan to Gaza and Israel, alongside record-breaking heat conditions, drought, wildfires and flooding. Societal discontent was palpable in many countries, with news cycles dominated by polarization, violent protests, riots and strikes.

Although globally destabilizing consequences – such as those seen at the initial outbreak of the Russia-Ukraine war or the COVID-19 pandemic – were largely avoided, the longer-term outlook for these developments could bring further global shocks.

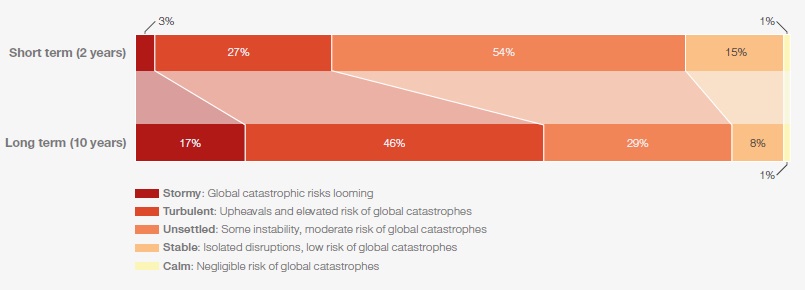

As we enter 2024, 2023-2024 GRPS results highlight a predominantly negative outlook for the world over the next two years that is expected to worsen over the next decade (Figure A). Surveyed in September 2023, the majority of respondents (54%) anticipate some instability and a moderate risk of global catastrophes, while another 30% expect even more turbulent conditions. The outlook is markedly more negative over the 10-year time horizon, with nearly two-thirds of respondents expecting a stormy or turbulent outlook.

In this year’s report, we contextualize our analysis through four structural forces that will shape the materialization and management of global risks over the next decade. These are longer-term shifts in the arrangement of and relationship between four systemic elements of the global landscape:

– Trajectories relating to global warming and related consequences to Earth systems (Climate change).

– Changes in the size, growth and structure of populations around the world (Demographic bifurcation).

– Developmental pathways for frontier technologies (Technological acceleration).

– Material evolution in the concentration and sources of geopolitical power (Geostrategic shifts).

FIGURE A – Short and long-term global outlook

“Which of the following best characterizes your outlook for the world over the following time periods?”

A new set of global conditions is taking shape across each of these domains and these transitions will be characterized by uncertainty and volatility. As societies seek to adapt to these changing forces, their capacity to prepare for and respond to global risks will be affected.

Environmental risks could hit the point of no return

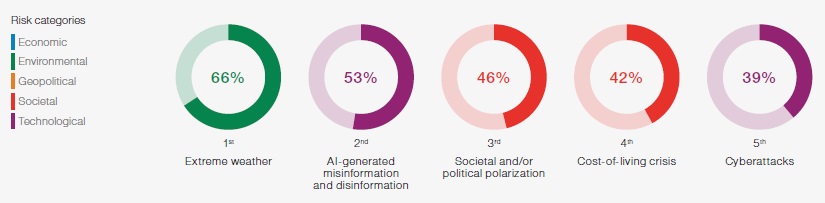

Environmental risks continue to dominate the risks landscape over all three time frames. Two-thirds of GRPS respondents rank Extreme weather as the top risk most likely to present a material crisis on a global scale in 2024 (Figure B), with the warming phase of the El Nino-Southern Oscillation (ENSO) cycle projected to intensify and persist until May this year. It is also seen as the second-most severe risk over the two-year time frame and similar to last year’s rankings, nearly all environmental risks feature among the top 10 over the longer term (Figure C).

However, GRPS respondents disagree about the urgency of environmental risks, in particular Biodiversity loss and ecosystem collapse and Critical change to Earth systems. Younger respondents tend to rank these risks far more highly over the two-year period compared to older age groups, with both risks featuring in their top 10 rankings in the short term. The private sector highlights these risks as top concerns over the longer term, in contrast to respondents from civil society or government who prioritize these risks over shorter time frames. This dissonance in perceptions of urgency among key decision-makers implies sub-optimal alignment and decision-making, heightening the risk of missing key moments of intervention, which would result in long-term changes to planetary systems.

Chapter 2.3: A 3oC world explores the consequences of passing at least one “climate tipping point” within the next decade. Recent research suggests that the threshold for triggering long-term, potentially irreversible and selfperpetuating changes to select planetary systems is likely to be passed at or before 1.5oC of global warming, which is currently anticipated to be reached by the early 2030s. Many economies will remain largely unprepared for “non-linear” impacts: the potential triggering of a nexus of several related socioenvironmental risks has the potential to speed up climate change, through the release of carbon emissions, and amplify related impacts, threatening climate-vulnerable populations. The collective ability of societies to adapt could be overwhelmed, considering the sheer scale of potential impacts and infrastructure investment requirements, leaving some communities and countries unable to absorb both the acute and chronic effects of rapid climate change.

FIGURE B – Current risk landscape

“Please select up to five risks that you believe are most likely to present a material crisis on a global scale in 2024.”

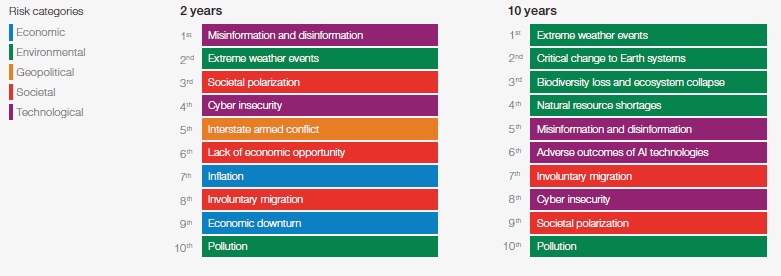

FIGURE C – Global risks ranked by severity over the short and long term

“Please estimate the likely impact (severity) of the following risks over a 2-year and 10-year period.”

As polarization grows and technological risks remain unchecked, ‘truth’ will come under pressure

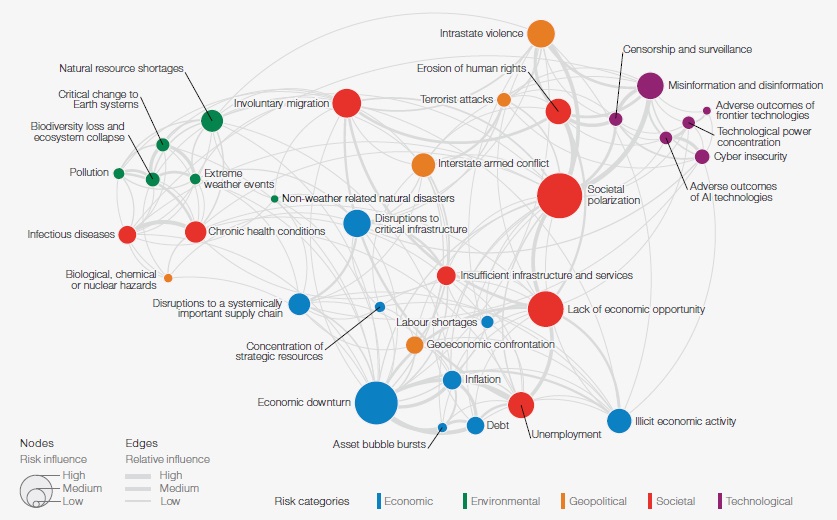

Societal polarization features among the top three risks over both the current and two-year time horizons, ranking #9 over the longer term. In addition, Societal polarization and Economic downturn are seen as the most interconnected – and therefore influential – risks in the global risks network (Figure D), as drivers and possible consequences of numerous risks.

Emerging as the most severe global risk anticipated over the next two years, foreign and domestic actors alike will leverage Misinformation and disinformation to further widen societal and political divides (Chapter 1.3: False information). As close to three billion people are expected to head to the electoral polls across several economies – including Bangladesh, India, Indonesia, Mexico, Pakistan, the United Kingdom and the United States – over the next two years, the widespread use of misinformation and disinformation, and tools to disseminate it, may undermine the legitimacy of newly elected governments. Resulting unrest could range from violent protests and hate crimes to civil confrontation and terrorism.

Beyond elections, perceptions of reality are likely to also become more polarized, infiltrating the public discourse on issues ranging from public health to social justice. However, as truth is undermined, the risk of domestic propaganda and censorship will also rise in turn. In response to mis- and disinformation, governments could be increasingly empowered to control information based on what they determine to be “true”. Freedoms relating to the internet, press and access to wider sources of information that are already in decline risk descending into broader repression of information flows across a wider set of countries.

FIGURE D – Global risks landscape: an interconnections map

The Cost-of-living crisis remains a major concern in the outlook for 2024 (Figure B). The economic risks of Inflation (#7) and Economic downturn (#9) are also notable new entrants to the top 10 risk rankings over the two-year period (Figure C). Although a “softer landing” appears to be prevailing for now, the near-term outlook remains highly uncertain. There are multiple sources of continued supply-side price pressures looming over the next two years, from El Nino conditions to the potential escalation of live conflicts. And if interest rates remain relatively high for longer, small- and mediumsized enterprises and heavily indebted countries will be particularly exposed to debt distress (Chapter 1.5: Economic uncertainty).

Economic uncertainty will weigh heavily across most markets, but capital will be the costliest for the most vulnerable countries. Climate-vulnerable or conflictprone countries stand to be increasingly locked out of much-needed digital and physical infrastructure, trade and green investments and related economic opportunities. As the adaptive capacities of these fragile states erodes further, related societal and environmental impacts are amplified.

Similarly, the convergence of technological advances and geopolitical dynamics will likely create a new set of winners and losers across advanced and developing economies alike (Chapter 2.4: AI in charge). If commercial incentives and geopolitical imperatives, rather than public interest, remain the primary drivers of the development of artificial intelligence (AI) and other frontier technologies, the digital gap between high- and low-income countries will drive a stark disparity in the distribution of related benefits – and risks. Vulnerable countries and communities would be left further behind, digitally isolated from turbocharged AI breakthroughs impacting economic productivity, finance, climate, education and healthcare, as well as related job creation.

Over the longer term, developmental progress and living standards are at risk. Economic, environmental and technological trends are likely to entrench existing challenges around labour and social mobility, blocking individuals from income and skilling opportunities, and therefore the ability to improve economic status (Chapter 2.5: End of development?). Lack of economic opportunity is a top 10 risk over the two-year period, but is seemingly less of a concern for global decision-makers over the longer-term horizon, dropping to #11 (Figure E). High rates of job churn – both job creation and destruction – have the potential to result in deeply bifurcated labour markets between and within developed and developing economies. While the productivity benefits of these economic transitions should not be underestimated, manufacturing – or services-led export growth might no longer offer traditional pathways to greater prosperity for developing countries.

The narrowing of individual pathways to stable livelihoods would also impact metrics of human development – from poverty to access to education and healthcare. Marked changes in the social contract as intergenerational mobility declines would radically reshape societal and political dynamics in both advanced and developing economies.

Simmering geopolitical tensions combined with technology will drive new security risks

As both a product and driver of state fragility, Interstate armed conflict is a new entrant into the top risk rankings over the two-year horizon (Figure C). As the focus of major powers becomes stretched across multiple fronts, conflict contagion is a key concern (Chapter 1.4: Rise in conflict). There are several frozen conflicts at risk of heating up in the near term, due to spillover threats or growing state fragility.

This becomes an even more worrying risk in the context of recent technological advances. In the absence of concerted collaboration, a globally fragmented approach to regulating frontier technologies is unlikely to prevent the spread of its most dangerous capabilities and, in fact, may encourage proliferation (Chapter 2.4: AI in charge). Over the longer-term, technological advances, including in generative AI, will enable a range of non-state and state actors to access a superhuman breadth of knowledge to conceptualize and develop new tools of disruption and conflict, from malware to biological weapons.

In this environment, the lines between the state, organized crime, private militia and terrorist groups would blur further. A broad set of non-state actors will capitalize on weakened systems, cementing the cycle between conflict, fragility, corruption and crime. Illicit economic activity (#31) is one of the lowest-ranked risks over the 10-year period but is seen to be triggered by a number of the top-ranked risks over the two – and 10-year horizons (Figure D). Economic hardship – combined with technological advances, resource stress and conflict – is likely to push more people towards crime, militarization or radicalization and contribute to the globalization of organized crime in targets and operations (Chapter 2.6: Crime wave).

The growing internationalization of conflicts by a wider set of powers could lead to deadlier, prolonged warfare and overwhelming humanitarian crises. With multiple states engaged in proxy, and perhaps even direct warfare, the incentives to condense decision time through the integration of AI will grow. The creep of machine intelligence into conflict decision-making – to autonomously select targets and determine objectives – would significantly raise the risk of accidental or intentional escalation over the next decade.

Ideological and geoeconomic divides will disrupt the future of governance

A deeper divide on the international stage between multiple poles of power and between the Global North and South would paralyze international governance mechanisms and divert the attention and resources of major powers away from urgent global risks.

Asked about the global political outlook for cooperation on risks over the next decade, twothirds of GRPS respondents feel that we will face a multipolar or fragmented order in which middle and great powers contest, set and enforce regional rules and norms. Over the next decade, as dissatisfaction with the continued dominance of the Global North grows, an evolving set of states will seek a more pivotal influence on the global stage across multiple domains, asserting their power in military, technological and economic terms.

As states in the Global South bear the brunt of a changing climate, the aftereffects of pandemic-era crises and geoeconomic rifts between major powers, growing alignment and political alliances within this historically disparate group of countries could increasingly shape security dynamics, including implications for high-stakes hotspots: the Russia-Ukraine war, the Middle East conflict and tensions over Taiwan (Chapter 1.4: Rise in conflict). Coordinated efforts to isolate “rogue” states are likely to be increasingly futile, while international governance and peacekeeping efforts shown to be ineffective at “policing” conflict could be sidelined.

The shifting balance of influence in global affairs is particularly evident in the internationalization of conflicts – where pivotal powers will increasingly lend support and resources to garner political allies – but will also shape the longer-term trajectory and management of global risks more broadly. For example, access to highly concentrated tech stacks will become an even more critical component of soft power for major powers to cement their influence. However, other countries with competitive advantages in upstream value chains – from critical minerals to high-value IP and capital – will likely leverage these economic assets to obtain access to advanced technologies, leading to novel power dynamics.

Opportunities for action to address global risks in a fragmented world

Cooperation will come under pressure in this fragmented, in-flux world. However there remain key opportunities for action that can be taken locally or internationally, individually or collaboratively – that can significantly reduce the impact of global risks.

Localized strategies leveraging investment and regulation can reduce the impact of those inevitable risks that we can prepare for, and both the public and private sector can play a key role to extend these benefits to all. Single breakthrough endeavors, grown through efforts to prioritize the future and focus on research and development, can similarly help make the world a safer place. The collective actions of individual citizens, companies and countries may seem insignificant on their own, but at critical mass they can move the needle on global risk reduction. Finally, even in a world that is increasingly fragmented, cross-border collaboration at scale remains critical for risks that are decisive for human security and prosperity.

The next decade will usher in a period of significant change, stretching our adaptive capacity to the limit. A multiplicity of entirely different futures is conceivable over this time frame, and a more positive path can be shaped through our actions to address global risks today.

FIGURE E – Global risks ranked by severity

“Please estimate the likely impact (severity) of the following risks over a 2-year and 10-year period.”

_________________________________________________

1 The report and an interactive data platform are available at https://www.weforum.org/publications/global-risks-report-2024/